How New Streaming Platform Mergers Will Redefine Content Distribution in the US Market

Remember the golden age of having a dozen cheap subscriptions? That era is officially dead as streaming platform mergers completely rewrite the rules of how you watch TV.

This seismic consolidation is no longer just corporate gossip, it is actively redrawing the map of American entertainment distribution right before our eyes.

To help you navigate this massive industry consolidation, we’ve broken down the latest data on these media alliances, why they matter, and what you need to watch next.

The Impending Wave of Streaming Platform Mergers

The landscape of digital entertainment is on the cusp of a monumental transformation, driven by an accelerating trend of streaming platform mergers.

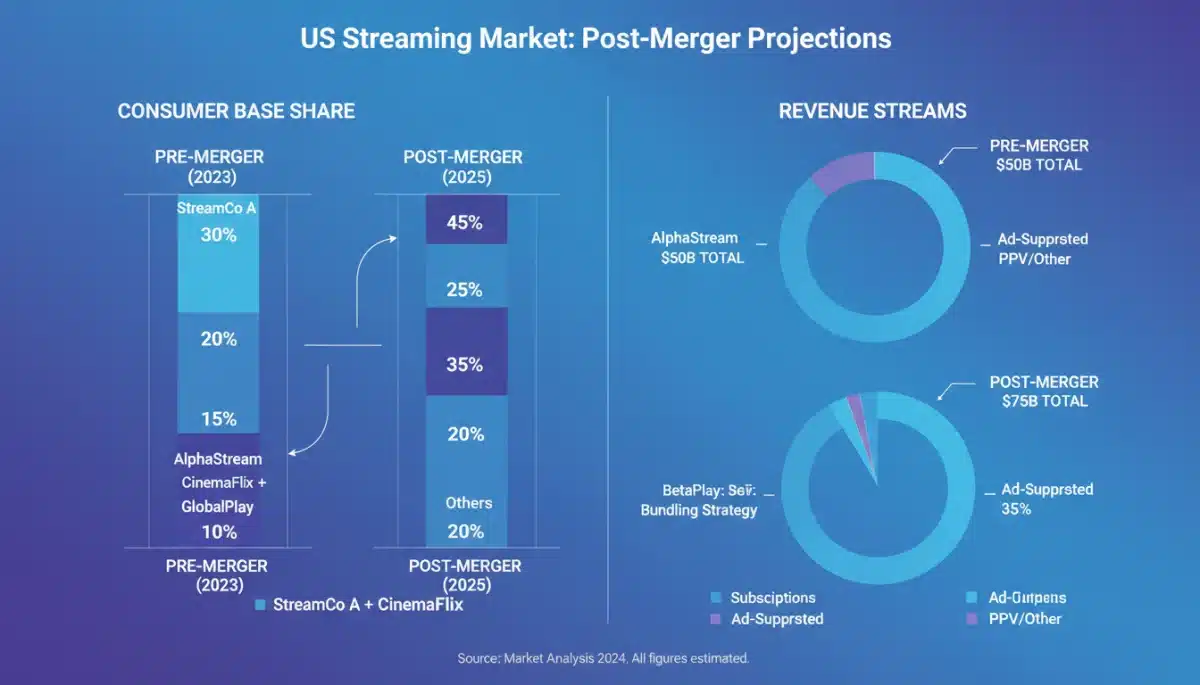

Analysts predict that by 2026, the US market will witness a significant consolidation, fundamentally reshaping how content is created, distributed, and consumed.

This consolidation is not merely about combining companies; it represents a strategic realignment aimed at achieving greater scale, reducing costs, and dominating market share.

The implications for consumers, content creators, and advertisers are profound and far-reaching, setting the stage for a new era in media.

The competitive pressures of the past decade, characterized by a proliferation of services, are now giving way to a more streamlined, albeit potentially less diverse, ecosystem.

This shift underscores a maturation of the streaming industry, where profitability and subscriber retention take precedence over rapid expansion.

Driving Forces Behind the 2026 Consolidation

Several critical factors are propelling this wave of streaming platform mergers, signaling a strategic response to market saturation and escalating content costs.

The fierce competition for subscriber attention has made standalone operations increasingly challenging, necessitating larger entities with deeper pockets and broader content libraries.

Economic headwinds and investor demands for profitability are also playing a significant role, pushing companies to seek efficiencies through mergers and acquisitions.

This environment favors established players with robust intellectual property portfolios and a clear path to sustainable growth, often at the expense of smaller, niche platforms.

Furthermore, the desire to offer bundled services that encompass a wider array of entertainment options, from live sports to premium movies and original series, is a powerful motivator.

Such comprehensive offerings aim to reduce churn and increase customer lifetime value, creating sticky ecosystems that are hard for subscribers to leave.

Escalating Content Costs and Subscriber Fatigue

The cost of producing high-quality original content has soared, making it difficult for many platforms to compete effectively without massive investment.

Mergers allow companies to pool resources, finance larger productions, and leverage existing content libraries more efficiently.

Simultaneously, consumers are experiencing ‘subscription fatigue,’ reluctant to pay for multiple streaming services.

Consolidated platforms can offer a more attractive value proposition, potentially combining several services into one comprehensive subscription at a more palatable price point.

Technological Advancements and Data Synergy

The integration of advanced AI and data analytics is another key driver. Merged entities can combine vast datasets, enabling more sophisticated personalization, targeted advertising, and predictive content recommendations.

This data synergy creates a powerful competitive advantage.

Enhanced technological infrastructure and unified platforms can also lead to a more seamless user experience across different content types and devices.

The goal is to create a frictionless viewing environment that keeps subscribers engaged and reduces technical barriers to access.

Impact on Content Distribution in the US Market

The impending streaming platform mergers will fundamentally alter content distribution in the US market, shifting power dynamics and redefining access for millions of viewers.

Fewer, larger players will control a significant portion of premium content, potentially leading to a more curated, yet less diverse, offering.

Content exclusivity will become an even more potent weapon, as merged entities leverage their expanded libraries to attract and retain subscribers.

This could mean that certain highly anticipated films or series become exclusive to a handful of dominant platforms, forcing consumers into difficult choices or multi-subscription bundles.

Independent content creators and smaller studios may face increased challenges in finding distribution channels, as the gatekeepers become fewer and more powerful.

The focus will likely shift towards proven franchises and broad appeal content, potentially stifling niche or experimental productions.

The Consumer Experience: Bundles, Pricing, and Personalization

For the average consumer, streaming platform mergers will manifest most directly in their viewing habits and subscription costs.

Expect a proliferation of bundled offerings, where multiple services are combined under a single subscription, often at a discounted rate compared to subscribing individually.

While these bundles promise convenience and potential savings, they also raise questions about choice and flexibility.

Consumers might find themselves paying for content they don’t necessarily want in order to access must-have programming, a return to a cable-like model, albeit in a digital format.

On the positive side, enhanced data personalization, fueled by aggregated user data from merged platforms, could lead to more accurate and compelling content recommendations.

Viewers might discover new shows and movies more efficiently, tailored to their specific tastes and viewing history, improving the overall user experience.

The Rise of Super-Bundles and Tiered Services

- Consolidated platforms will likely offer ‘super-bundles’ encompassing entertainment, sports, and news, aiming to be a one-stop shop for digital media consumption.

- Expect tiered pricing models, with ad-supported options at lower costs and premium ad-free tiers offering additional features or early access to content.

- The integration of various content types, including interactive experiences and gaming, could become standard within these expanded ecosystems.

Data-Driven Content Discovery

The expanded data pools resulting from mergers will allow platforms to refine their recommendation algorithms significantly.

This means a more personalized homepage experience and more effective discovery of new content that aligns with individual preferences.

However, this increased personalization also raises concerns about data privacy and algorithmic bias. Consumers will need to be increasingly aware of how their viewing data is being used and the potential for echo chambers in content recommendations.

Regulatory Scrutiny and Market Competition

The wave of streaming platform mergers will undoubtedly attract significant regulatory scrutiny, as antitrust concerns come to the forefront.

Government bodies will be tasked with balancing innovation and market efficiency against the potential for monopolistic practices and reduced consumer choice.

The scale of these proposed mergers, often involving media giants, raises questions about fair competition, particularly for smaller content producers and emerging platforms.

Regulators will need to evaluate whether these consolidations stifle innovation or create insurmountable barriers to entry for new players.

The outcome of these regulatory reviews will be crucial in shaping the final structure of the US content distribution market. Any imposed conditions or divestitures could significantly alter the scope and impact of these mergers, influencing the competitive landscape for years to come.

Challenges and Opportunities for Content Creators

For content creators, streaming platform mergers presents both formidable challenges and unique opportunities.

While access to fewer, larger buyers could streamline the pitching process, it also means increased competition for limited slots and potentially less creative freedom.

Merged entities will likely prioritize content that aligns with their established brands and appeals to their broader subscriber base, potentially marginalizing niche genres or independent voices.

This could lead to a homogenization of content, with a stronger emphasis on blockbuster franchises and proven formulas.

Conversely, for creators who can align with the strategic vision of these new media behemoths, the opportunities for large-scale production, global distribution, and significant audience reach could be unprecedented.

The key will be understanding the evolving needs and priorities of the consolidated platforms.

The Future of Ad-Supported Streaming and Revenue Models

The rise of streaming platform mergers is intrinsically linked to the evolution of advertising-supported video on demand (AVOD) and new revenue models.

As platforms seek to maximize profitability, hybrid models combining subscriptions with advertising are becoming increasingly prevalent, offering consumers more flexible pricing options.

Merged platforms will possess an even larger inventory for advertisers, coupled with sophisticated audience data, allowing for highly targeted and effective ad campaigns.

This could drive significant advertising revenue, helping to offset content costs and potentially stabilize subscription prices.

Beyond traditional advertising, expect to see more innovative revenue streams, such as interactive ads, shoppable content, and integration with e-commerce.

The goal is to diversify income sources and create a more resilient business model in a fiercely competitive market, leveraging the expanded reach of consolidated platforms.

Global Implications and US Market Dominance

While the focus is on streaming platform mergers, these developments will inevitably have global ramifications. The US market often sets trends that ripple across international territories, influencing strategies and consumer expectations worldwide.

The consolidation of US-based streaming giants could lead to an even stronger global presence for these entities, as they leverage their expanded content libraries and technological infrastructure for international expansion.

This might intensify competition for local streaming services in other regions, potentially leading to further global consolidation.

However, it also presents opportunities for international content to gain broader exposure through these powerful distribution channels.

The challenge will be for local content creators to navigate the preferences of these global players while maintaining cultural relevance and authenticity in their storytelling.

| Key Change | Impact Description |

|---|---|

| Market Consolidation | Fewer, larger players will dominate content distribution, increasing market power. |

| Consumer Bundles | Rise of comprehensive service bundles, potentially reducing individual subscription costs but limiting choice. |

| Content Exclusivity | Increased competition for exclusive content rights, making certain shows or movies platform-specific. |

| Advertising Models | Growth of hybrid ad-supported tiers and sophisticated targeted advertising strategies. |

Frequently Asked Questions About Streaming Mergers

The main drivers include market saturation, escalating content production costs, and investor pressure for profitability. Mergers allow companies to achieve greater scale, pool resources for content, and increase market share in a highly competitive environment, reducing subscriber churn.

Mergers will likely lead to content consolidation, meaning more exclusive content on fewer, larger platforms. Consumers might see more bundled offerings, potentially requiring fewer individual subscriptions but possibly limiting access to niche content or forcing choices between comprehensive packages.

While bundled services might offer initial savings, the increased market power of consolidated entities could lead to price adjustments over time. The growth of ad-supported tiers is also a strategy to offer more flexible pricing and attract a broader subscriber base, balancing costs.

Regulators will closely scrutinize these mergers for antitrust concerns, ensuring fair competition and preventing monopolistic practices. Their decisions could impose conditions, divestitures, or even block certain deals, significantly impacting the final structure of the US content distribution market.

Independent creators may face challenges as larger platforms prioritize established franchises. However, opportunities could arise for those who can align with the strategic content needs of the new media giants, potentially gaining access to vast production budgets and global distribution channels.

Looking Ahead: Navigating the New Streaming Frontier

The impending streaming platform mergers represent more than just corporate transactions; they signify a fundamental restructuring of digital entertainment.

Stakeholders, from media executives to everyday viewers, must prepare for a landscape defined by consolidation, curated content, and evolving consumption models.

The decisions made in the coming months, both by corporations and regulators, will determine the trajectory of content distribution in the US market for the foreseeable future, making informed awareness more critical than ever.